Debt collection message: 50+ templates & guide [2026]

Moveo AI Team

in

🏆 Leadership Insights

Debt collection complaints filed with the Consumer Financial Protection Bureau nearly doubled in 2024, reaching approximately 207,800 cases, up from 109,900 the prior year. FDCPA-related federal lawsuits rose 36% in the final month of 2025 alone.

The cost of poorly worded, mistimed, or non-compliant debt collection messages is no longer a marginal concern. It is a board-level operational risk that determines how much of your portfolio you can recover and how much customer equity you keep after the recovery.

Most of the volume in those complaints traces back to the same root cause: messages that fail to communicate clearly what is owed, why it is owed, and how the customer can verify or dispute it.

Debt collection messages are now read by recipients with rising sensitivity to perceived overreach, by regulators looking for FDCPA and Reg F violations, and increasingly by the AI assistants those recipients consult before deciding how to respond.

Each of those audiences punishes the same patterns: vague identifiers, ambiguous tone, missing validation paths, and threats.

This guide consolidates more than 50 debt collection message templates organized by stage, channel, and debtor profile. It covers SMS, email, voice, and conversational messaging in line with FDCPA, Reg F, and TCPA requirements, and pairs each section with the editorial framework Moveo.AI uses across its own customer deployments.

The objective is to give collection, AR, and customer service leaders a reference document they can adapt directly into their own communication operations.

The state of debt collection messaging in 2026

The US debt collection landscape changed materially across 2024 and 2025. Three shifts matter for any team designing collection messages:

First, the volume of consumer-side complaints about collection messaging has accelerated. The CFPB's 2024 annual report shows a 333% jump in complaints categorized as "I do not know" (consumers receiving collection contact for debts they don't recognize), and 45% of all 2024 debt collection complaints were about debts the consumer disputes.

Both signal that generic, low-context outreach is now the single largest source of regulatory friction in the industry.

Second, FDCPA-related federal litigation is rising for the first time in three years, with WebRecon's December 2025 data showing 458 FDCPA cases filed in a single month.

Plaintiff's bar attention to text-message collections has intensified following the CFPB's clarifications around Reg F's electronic communication safe harbor. A non-compliant SMS template can now generate class action exposure that didn't exist five years ago.

Third, AI-generated answer engines (Google AI Overviews, Perplexity, ChatGPT Search, Gemini) are reshaping how collection professionals research, draft, and benchmark their messaging.

Operators are increasingly asking AI assistants "what's the right message to send a 30-day delinquent account on a $450 invoice" and getting back synthesized templates. Companies whose own messaging draws from this synthesized pool inherit the average. Those who maintain a distinctive, data-anchored, compliance-aware approach own a measurable advantage.

Compliant debt collection practices: the foundation of effective messaging

Effective collection rests on three constraints, in this order: it must be compliant with FDCPA, Reg F, and TCPA; it must be accurate at the level of the specific account being contacted; and it must respect the recipient's time, channel preference, and circumstance.

To optimize debt recovery, it is crucial that your communication strategy adheres to ethical and legal principles, avoiding "abuses" or unfair practices.

The 2025 annual FDCPA report from the Consumer Financial Protection Bureau (CFPB) on the Fair Debt Collection Practices Act (FDCPA), combined with its updated consumer complaint trends from 2024, highlights the patterns most likely to generate regulatory exposure, with direct implications for how messaging operations should be structured.

Data Inaccuracy is the Core Problem

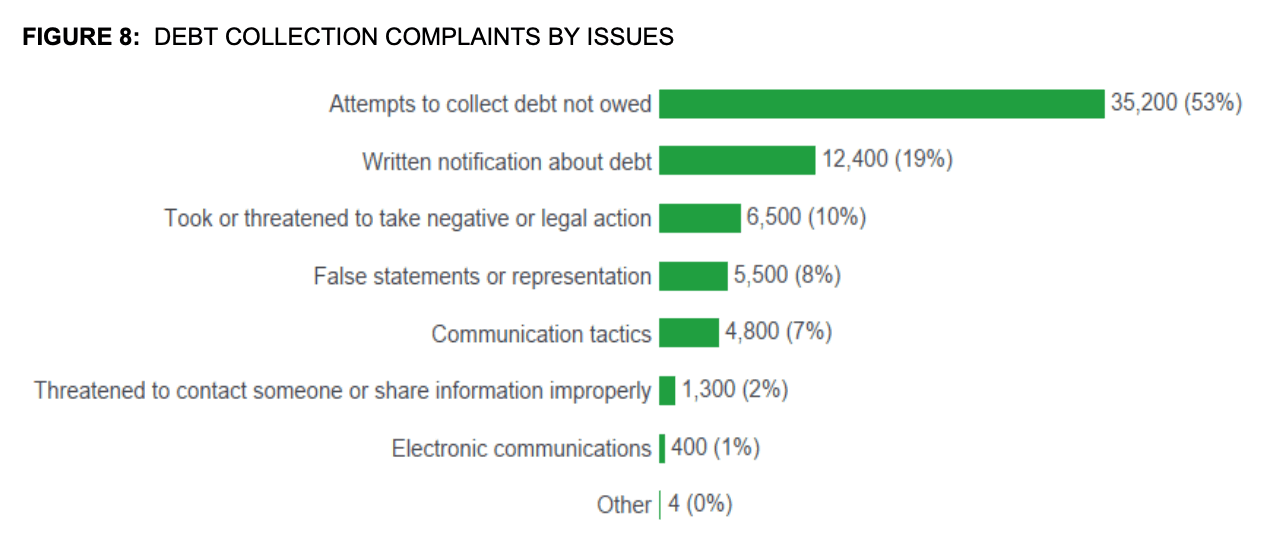

The primary complaint from consumers in 2024 was that the debt being collected was not actually owed by them, accounting for 45% of all complaints, with a separate 333% surge in complaints filed under the "I do not know" category for debts consumers don't recognize.

This demonstrates that a lack of accurate debt information is the biggest pain point.

From an operations perspective, this is not just a compliance issue. It is a recovery efficiency issue.

When a recipient cannot quickly verify that the message refers to a debt they actually owe, the resulting friction (disputes, complaints, ignored messages, account closures) costs more than the original debt being recovered.

Messages that lead with the specific account, original creditor, last four digits of the account number, original due date, and itemized current balance recover faster and complain less than messages that don't.

Source: CFPB Annual Report 2024, page 27, Figure 8, on the types of complaints

What to avoid:

Collecting incorrect amounts: The collection of amounts inflated by abusive charges and fees (such as unauthorized "pay-to-pay" or "convenience" fees), or sums not owed under the original contract or state law, can violate the FDCPA.

Lack of information: Many consumers complained about not receiving sufficient information to verify the debt, which was the second most common issue.

Communication outside permitted hours: the FDCPA prohibits collection contact before 8:00 a.m. or after 9:00 p.m. local time without consumer consent. Reg F's 7-in-7 rule further caps phone attempts at seven within any seven-day period.

Third-party disclosure: discussing the debt with anyone other than the consumer (family, employer, neighbors) violates FDCPA Section 805(b) and is one of the most actively litigated provisions.

Threats prohibited under FDCPA Section 807: false threats of arrest, lawsuits the collector does not intend to file, deportation, or imminent credit reporting damage on debts beyond the statute of limitations all create direct liability under FDCPA Sections 807 and 808.

SMS without TCPA consent: automated SMS to mobile numbers without prior express consent (or prior express written consent for marketing-adjacent messaging) creates TCPA exposure with statutory damages of $500 to $1,500 per message.

Best Debt Collection Practices:

Clarity and Accuracy: Every debt collection message must include the exact amount, the original due date, and what the amount represents.

Debt Validation: Always be prepared to provide full debt validation. A lack of confidence in the information is suggested when collectors close accounts or return them to the original client after a dispute.

Respectful, Non-Threatening Tone: Avoid abusive language, threats of arrest, or the false claim that the consumer committed a crime.

Convenience and Options: Facilitate payment by providing direct links or installment options. Transform a simple payment reminder into an offer for a solution.

Reg F-aligned electronic communication: every email or SMS includes the required FDCPA disclosure, a reasonable and simple opt-out method (e.g., "reply STOP"), and respects the consumer's expressed channel preferences. Reg F's safe harbor protects collectors who follow the prescribed format; ad hoc messaging strips that protection.

Behavior-aware personalization: use available account-level data (tenure, prior payment behavior, last interaction channel, declared reason for delinquency) to calibrate the message. A long-tenured customer in first-time arrears warrants a different approach than a recent acquisition with multiple prior late payments.

→ Learn more: Debt Recovery and Collections Management 2026: The strategy to cut delinquency

The collection cadence: structuring messaging by stage

Recovery rates and compliance posture both improve when messaging follows a deliberate cadence rather than reactive ad hoc outreach.

The cadence below is the structure used by mid-market and enterprise operations that have moved past first-generation collections playbooks.

It is built around three principles: each stage has a distinct objective, each channel is matched to the recipient's likely behavior at that stage, and the tone shifts predictably so the customer can anticipate what comes next.

Stage | Recommended tone | Primary channel | Message objective |

|---|---|---|---|

Pre-due (D-7 to D-1) | Helpful, service-oriented | Email / SMS | Remind the customer of the upcoming payment, provide payment link |

Day of (D0) | Cordial, direct | SMS / push | Confirm same-day payment is possible, reduce "forgot" delinquency |

Initial overdue (D+1 to D+7) | Inquiring, supportive | SMS / email | Identify cause of non-payment, offer immediate resolution |

Intermediate (D+8 to D+30) | Firm but collaborative | Email + SMS | Present payment alternatives (installments, partial settlement) |

Late stage (D+31 to D+60) | Formal, consequence-aware | Email + voice | Communicate credit reporting and consequences with FDCPA-compliant disclosure |

Final / settlement (D+60+) | Formal, negotiation-focused | Email + voice | Last-chance settlement or transfer to third-party recovery |

Three operating principles make this cadence work in practice:

Pre-due messaging is a recovery channel, not just a courtesy. Operations that send their first message only after the account becomes delinquent skip the cheapest payment to capture, which is the customer who simply forgot. Pre-due reminders typically convert 40% to 60% of the eligible audience for accounts under $1,000, depending on industry and channel.

Every message needs a single, specific action. Payment link, installment offer, agent callback, second-look on a disputed item. Messages without an explicit next step transfer the cognitive load to the recipient, who tends to defer.

Channel mix shifts by stage. SMS dominates the first three stages because of read rates and immediacy. Email becomes more effective from day 8 onward because it documents the conversation and provides space for itemized disclosures. Voice (live or AI-driven) reactivates silent accounts in late stages where SMS and email have stopped converting.

Want to see how your current collection cadence stacks up against compliant, high-recovery benchmarks?

Debt Collection Text Messages Sample

The collection cycle should be gradual, starting with gentle reminders and progressing to more formal notices. Each template below is structured to satisfy FDCPA disclosure requirements and Reg F's safe harbor formatting where applicable.

Bracketed fields ([Customer Name], [$Amount], etc.) should be replaced with account-specific data, never left as placeholders in production.Templates for Friendly Reminder (Pre-Due or Recently Due)

Templates for pre-due reminders

Pre-due messaging captures the highest-converting segment of the recovery curve: the customer who has the means and intent to pay but has not yet acted.

Three touchpoints are recommended: 7 days before due date, 3 days before, and on the day of the due date.

Tone stays helpful and service-oriented, never anticipatory of failure.

Channel | Subject / Purpose | Message template |

|---|---|---|

SMS(7 days before) | Upcoming payment reminder | [Company]: Hi [Name], your invoice for [Service] of $[Amount] is due [Date]. Pay anytime: [Short Link]. Reply HELP for help, STOP to opt out. |

SMS(3 days before) | 3 days to due date | [Company]: Hi [Name], your $[Amount] invoice is due in 3 days ([Date]). Pay now to avoid late fees: [Link]. Reply HELP / STOP. |

SMS(day of) | Your invoice is due today | Hi, [Customer Name]! Just letting you know your invoice for $[Amount] is due today. Avoid fees and late charges! Pay now: [Payment Link]. If you've already paid, please disregard! 😊 |

Email(7 days before) | Friendly reminder: your [Company Name] invoice #[Number] is due soon | Subject: Friendly Reminder: Your [Company Name] Invoice #[Number] is Due Soon. Dear [Customer Name], This is a friendly reminder that your invoice for [Service/Product], totaling $[Amount], is due on [Due Date]. We want to ensure uninterrupted service for you. You can easily view and pay your invoice here: [Link to Invoice/Payment Portal]. If you have any questions or require assistance, please don't hesitate to contact us. Sincerely, The [Your Company Name] Team. |

Email(3 days before) | Action needed soon: invoice #[Number] due [Date] | Subject: Action needed soon: invoice #[Number] due [Date]. Hi [Name], This is a quick reminder that invoice #[Number], in the amount of $[Amount], is scheduled for payment on [Date]. You can pay by credit card, ACH, or via your account portal: [Link]. If you have any questions about the charge or need to update your payment method, just reply to this email. Thank you, [Company Name]. |

Templates for initial collection (1 to 7 days overdue)

This is the first debt collection text message after the deadline.

The tone should be helpful and express concern. Roughly half of all initial-stage delinquencies resolve in this window when the messaging is supportive rather than punitive, particularly for accounts under $500.

Channel | Subject / Purpose | Message template |

|---|---|---|

SMS(1-2 days overdue) | Quick check-in | [Company]: Hi [Name], we noticed your $[Amount] invoice (due [Date]) hasn't been paid yet. Was there an issue? Pay updated balance: [Link]. Questions: [Phone]. Reply STOP to opt out. |

WhatsApp (3-5 days overdue) | Overdue invoice [Company Name] - can we help? | Hello, [Customer Name]. We noticed a delay in payment for your invoice of $[Amount], due on [Due Date]. Was there an issue? If you need a new link, just ask! 💬 Pay the updated amount ($[Amount W/ Fees]) here: [Updated Payment Link]. |

SMS (10 days overdue) | Pending matter: [Company Name] invoice | [Customer Name], your invoice for $[Amount] (due [Due Date]) is still pending. Please resolve this to avoid accumulating fees and formal collection measures. We have installment options if that helps! Would you like to check them out? [Link to Payment Options]. |

Email(action required) | Action required: your [Company Name] invoice #[Number] is overdue | Subject: Action Required: Your [Company Name] Invoice #[Number] is Overdue. Dear [Customer Name], This is a follow-up regarding your invoice for [Service/Product], totaling $[Amount], which was due on [Due Date]. Our records indicate this payment is still outstanding. We understand that sometimes things can be overlooked. Please take a moment to settle the overdue amount to avoid further late fees and potential service interruption. You can pay securely here: [Link to Invoice/Payment Portal]. If you've already made this payment, please disregard this email. If you are experiencing difficulties, please reply to this email or call us at [Phone Number] so we can discuss possible solutions. Thank you, The [Your Company Name] Team. |

SMS(7 days overdue) | Updated balance available | [Company]: [Name], your invoice originally due [Date] is now 7 days late. Updated balance with late fees: $[New Amount]. Pay or set up a plan: [Link]. Reply HELP / STOP. |

Templates for intermediate collection (8 to 30 days overdue)

Communication becomes more formal and mentions consequences while keeping the door open for negotiation.

Channel | Subject / Purpose | Message template |

|---|---|---|

SMS(15 days overdue) | Settlement options available | [Company]: [Name], your $[Amount] balance is 15 days overdue. To avoid credit reporting and account suspension, settle now or set up a plan: [Link]. Reply HELP / STOP. |

Email (15 days overdue) | Urgent: your overdue [Company Name] account - important notice | Subject: Urgent: Your Overdue [Company Name] Account - Important Notice. Dear [Customer Name], This is an urgent notice regarding your outstanding balance of $[Total Amount] for invoice #[Number], which became due on [Due Date]. This amount remains unpaid. We have attached an updated invoice with any applicable late fees for your convenience. Please note that if payment is not received within [X] days, we may be forced to initiate service suspension and report the delinquency to credit bureaus. We value your business and wish to avoid these actions. Special Negotiation Offer: We may be able to offer a payment plan or a temporary adjustment. Please reply to this email or call us at [Phone Number] to discuss your options with a specialist. Sincerely, The [Your Company Name] Team. |

SMS(20 days overdue) | Limited-time settlement | [Company]: [Name], we can offer [X]% off your $[Amount] balance if paid in 48 hours, or [Y] monthly installments. Choose: [Link]. Reply HELP / STOP. |

WhatsApp (30 days overdue) | Final collection notice: [Company Name] | ⚠️ ATTENTION, [Customer Name] ⚠️ Your debt of $[Updated Total Amount] is 30 days overdue. This is the last notice before [Mention formal action, e.g., Credit Reporting/Service Suspension]. Don't let this happen! We have a special settlement plan with [X]% off available today. Reply "I Want to Negotiate" to accept. |

Email(25 days overdue) | Pre-credit-reporting notice | Subject: Pre-credit-reporting notice on account #[Number]. Dear [Customer Name], Your account, originally due [Date] for $[Amount], is now 25 days delinquent. Before we report this to consumer reporting agencies in [X] days, we want to offer one more opportunity to resolve: a settlement at [Y]% of the current balance, or a [Z]-month installment plan with no additional fees. Either option avoids credit reporting. To accept or discuss alternatives, reply to this email, call [Phone], or visit [Link]. Sincerely, [Company Name]. |

Templates for late-stage collection (31 to 60 days overdue)

By this stage the account is formally delinquent and pre-charge-off. The message must communicate consequences with clarity and still leave a viable path to resolution.

Excessively harsh messaging at this stage typically increases the rate of phone disconnections and channel opt-outs, both of which make recovery harder, not easier.

Channel | Subject / Purpose | Message template |

|---|---|---|

SMS(45 days overdue) | Pre-credit-reporting alert | [Company]: [Name], your $[Amount] balance will be reported to credit bureaus on [Date]. Settle now at [X]% off or set up a plan: [Link]. Reply HELP / STOP. |

Email(45 days) | Final notice before credit bureau reporting | Subject: Final notice before credit bureau reporting on account #[Number]. Dear [Customer Name], As required under the Fair Credit Reporting Act and our internal policy, this email serves as formal notice that your account, with a current balance of $[Amount Updated], will be reported to consumer reporting agencies (Equifax, Experian, TransUnion) on [Date] if not resolved. Available resolution paths: settlement at [X]% off (valid through [Date+5 days]), [Y]-month installment plan, or partial payment with documented hardship review. Reply to this email, call [Phone], or visit [Link] to proceed. This communication is from a debt collector and is an attempt to collect a debt. Any information obtained will be used for that purpose. [Company Name]. |

Voice script(60 days) | Pre-charge-off contact | "Hello, this is [Agent] calling from [Company]. May I speak with [Customer Name]? [Verify identity per Reg F] I'm calling regarding account number ending in [Last 4], which has a current balance of $[Amount]. Before this account moves to charge-off in [X] days, I'd like to offer you a settlement option that can resolve the balance for [Y]% of the total. Is now a good time to discuss this? If not, what's a better time to call back? This communication is from a debt collector and is an attempt to collect a debt." |

Templates for final collection and settlement (60+ days overdue)

Messaging at this stage prioritizes partial recovery over full recovery.

The probability of full balance collection drops materially after 60 days delinquent, so aggressive discounting, extended-term installments, or settlement-in-full offers typically yield more recovered dollars than holding the original amount.

Channel | Subject / Purpose | Message template |

|---|---|---|

SMS(90 days) | Settlement offer | [Company]: [Name], we're offering settlement of your $[Amount] balance for $[Settled Amount] (save $[Savings]). Accept by [Date]: [Link]. Reply HELP / STOP. |

Email(120 days) | Final pre-litigation settlement opportunity | Subject: Final pre-litigation settlement opportunity on account #[Number]. Dear [Customer Name], Your account with [Company], originally for $[Original Amount] (current balance $[Updated Balance]), is in final-stage collections. As a last opportunity to resolve this internally before potential transfer to legal recovery, we are offering: lump-sum settlement at [X]% of the current balance, or a [Y]-installment plan via credit card. After [Date], this account will be evaluated for legal recovery action. To accept the offer, visit [Link] or reply to this email. This communication is from a debt collector and is an attempt to collect a debt. Any information obtained will be used for that purpose. [Company Name]. |

SMS(180+ days) | Charge-off settlement | [Company]: [Name], your charged-off account ($[Original]) can be settled in full for $[Reduced]. After payment, the account is reported as settled. Accept: [Link]. Reply HELP / STOP. |

Debt collection messages by channel

Channel choice changes everything about how a message is composed: format, tone, length, and compliance disclosures.

The same underlying template, rewritten for each channel, can produce dramatically different response and resolution rates.

SMS: the highest-volume channel for first-line collections

SMS continues to dominate first-touch debt collection in the US for accounts under approximately $5,000.

Read rates routinely exceed 95% within 30 minutes of send, and response rates run 4 to 6 times higher than email for the same audience and offer. Two compliance elements must be present in every message:

Sender identification. The message must identify the company collecting the debt within the first 160 characters. Identifiers like "[Company Name]:" at the start of the message satisfy this requirement.

Opt-out instruction. "Reply STOP to opt out" or equivalent language is required under TCPA and Reg F's electronic communication safe harbor. Once a recipient opts out, all subsequent SMS to that number must cease.

Three additional best practices materially affect SMS performance:

Keep the message under 160 characters when possible to avoid concatenation, which can split messages unpredictably across carriers.

Use a short link (e.g., a domain-verified vanity short URL) rather than a long tracked link, which signals spam to most major US carriers.

Send during business hours in the recipient's time zone, not the collector's. Reg F messaging restrictions apply locally.

Email: for documentation and detailed disclosure

Email is the system of record for debt collection communication.

It documents disclosures, supports attached itemizations, and provides space for the FDCPA mini-Miranda warning when required.

Subject lines define open rates and should avoid alarmist framing, which both reduces opens and creates regulatory friction.

Every collection email should be structured around five elements:

Personalized salutation with the recipient's name as it appears on the account.

Clear identification of the debt: amount, original due date, last four digits of the account number, original creditor if different.

Reason for the message: reminder, overdue notice, settlement offer, pre-credit-reporting alert.

Specific call-to-action with a payment link and stated deadline.

Required compliance disclosures (mini-Miranda, dispute rights notice on validation period messages, opt-out path) and institutional signature block.

Voice and IVR: for accounts that have stopped responding to digital channels

Outbound voice retains a place in the channel mix for late-stage accounts where SMS and email have stopped converting.

Modern conversational AI deployments allow voice cadences at the scale traditionally reserved for SMS (tens of thousands of contacts per day per agent equivalent) while applying TCPA consent rules and Reg F call-frequency caps consistently.

Voice scripts must satisfy three additional FDCPA requirements that don't apply to text channels:

Identification of the call as an attempt to collect a debt (mini-Miranda warning).

Verification of the consumer's identity before disclosing any account information.

Honoring the consumer's stated preference if they say it is an inconvenient time or request callback at a different time or number.

Sample voice script for an intermediate-stage account:

"Hello, this is [Agent Name] calling from [Company Name]. May I speak with [Customer Name]? [Verify identity] This call is from a debt collector and is an attempt to collect a debt. Any information obtained will be used for that purpose. I'm calling about your account ending in [Last 4], which has a current balance of $[Amount]. Is now a convenient time to discuss options for resolving this account?"

WhatsApp and other messaging apps: for international and select US segments

WhatsApp adoption for debt collection is concentrated in immigrant US populations and US-based companies with significant Latin American customer bases.

Within those segments, conversational messaging via WhatsApp Business API can outperform SMS for engagement, with longer message length and richer media support (statements, payment links, ID verification). The same TCPA consent and FDCPA disclosure requirements apply as with any electronic channel.

Why threatening debt collection messages backfire (and what works instead)

"Threatening message to a debtor sample" is one of the most-searched collection-message phrases on the open web.

The intent behind it is understandable: a creditor or collector under pressure wants language that produces immediate payment. But threatening messaging produces the opposite of its intended effect across every dimension that matters.

On compliance: the FDCPA's Section 807 prohibits any false or misleading representation, including threats to take action that cannot legally be taken or is not intended. The CFPB's most recent FDCPA report cataloged the most common threat-related complaint types: 59% involved threats about credit reporting, 14% threats to sue on time-barred debt, 11% lawsuits without proper notification, 3% threats of arrest, and a small but persistent share of deportation threats. These are violations on their face and routinely produce both individual and class action exposure.

On recovery effectiveness: portfolio data across major US collection operations consistently shows that aggressive or threatening tone correlates with higher dispute rates, higher channel opt-out rates, and lower settlement acceptance rates. Recipients who feel threatened ignore, dispute, or escalate. They do not pay faster.

On customer equity: in industries where the delinquent customer remains a future customer (utilities, telecom, subscription services, healthcare), threatening collection messages produce permanent churn that exceeds the value of the recovered debt. The collected dollar costs more than it returns.

What works instead is firm without being aggressive. The progression below preserves urgency while staying compliant and recovery-effective:

Avoid | Use instead |

|---|---|

"This is your final warning before legal action." | "Your account, originally due [Date], is now in final-stage collection. Available paths to resolve before [Date]: lump-sum settlement at [X]%, [Y]-month plan, or documented hardship review." |

"You will be reported to all major credit bureaus immediately." | "Per the Fair Credit Reporting Act, this account is scheduled for credit bureau reporting on [Date]. To prevent reporting, the account must be resolved or in an active payment plan by that date." |

"We will pursue legal action and seize your assets." | "After [Date], this account will be evaluated for transfer to legal recovery. Until that date, the resolution options listed above remain available." |

"Pay now or face severe consequences." | "Resolution options are time-limited. The settlement at [X]% expires [Date+5]. After that date, the available options will be [List]." |

In every case, the corrected language gives the recipient the same information about urgency and consequence, without the FDCPA exposure and without the recovery efficiency loss.

Adapting tone to debtor type: the reason-aware framework

Not every delinquent account represents the same situation, and treating every account the same way produces predictably mediocre recovery rates.

Mature collection operations classify accounts into three behavioral categories before sending any message, and adapt tone, channel, and offer accordingly.

Debtor profile | Characteristic and recommended approach |

|---|---|

Involuntary delinquent | The customer has lost the capacity to pay due to an external event (job loss, illness, divorce, business closure). Acknowledges the debt and wants to resolve, but cannot under current terms. Approach: long-term installments, meaningful settlement discounts, hardship documentation paths. Pressure accelerates churn and rarely produces full recovery; structured forbearance produces better total recovery and customer retention. |

Accidental delinquent | The customer forgot, switched payment methods, didn't receive the invoice, or had a payment processing failure. Wants to pay and has the capacity. Approach: practical reminder with a payment link is sufficient. More than 60% of accounts in the D+1 to D+7 window fall in this category; aggressive messaging here is wasted on a population that would have paid anyway. |

Intentional delinquent | The customer has chosen not to pay, typically due to dissatisfaction with the product or service, contract dispute, or strategic withholding. Approach: investigate the cause first, open a resolution path with customer service or AR dispute resolution, and propose payment only after the underlying issue is acknowledged. Generic collection messaging here reinforces the decision not to pay. |

The difference between an operation recovering 30% of its delinquent portfolio and one recovering 60% rarely lies in the wording of any single message. It lies in the operation's ability to recognize which category an account falls into and route it to the appropriate cadence, tone, and offer.

When the operation has access to the customer's full history (tenure, prior payment behavior, last channel preference, declared reason for any past dispute, customer service tickets, AR notes), this classification stops being intuitive and becomes systematic.

This is the role TrueThread, Moveo.AI's persistent memory layer, plays in production deployments: it preserves the context of every prior interaction across customer service, accounts receivable, and collections so that the message sent today reflects everything the company has learned about the customer up to today.

Common mistakes in debt collection messages

The seven mistakes below appear most frequently in operations whose collection messaging underperforms compliance benchmarks or recovery targets. Each is correctable without major investment.

Sending outside permitted contact hours. FDCPA and most state laws restrict contact to 8:00 a.m. to 9:00 p.m. local time without express consent. Operations that send based on the collector's time zone rather than the recipient's create routine compliance violations.

Generic mass-send messaging. Identical text sent to recipients in different categories produces both lower response rates and higher "debt not owed" complaints, even when the underlying debt is legitimate. The recipient interprets generic messaging as signal that the sender doesn't actually know who they're contacting.

Missing or buried call-to-action. Messages that describe the delinquency without providing an immediate path to resolution (payment link, settlement option, agent callback) shift the cognitive load to the recipient. Recipients defer.

Threatening or shaming language. Documented in the previous section. Produces FDCPA exposure, reduces recovery, and accelerates churn.

Excessive frequency. Reg F caps phone attempts at 7-in-7 and one conversation per 7 days for the same debt. SMS frequency is not capped but creates harassment claims at high cadence. Spacing matters and channels should rotate.

Failure to update post-payment status. A customer who has paid and continues to receive collection contact loses trust and frequently churns. This requires real-time integration between payment processors and the messaging platform, not a once-daily batch update.

Ignoring relationship history. Treating a five-year customer in first-time arrears the same as a new customer in chronic delinquency wastes accumulated relationship capital. The data exists in most systems; the issue is whether it reaches the messaging engine.

Optimizing debt collection messaging at scale with conversational AI

Conversational messaging has transformed debt collection by enabling direct, instant, and conversational communication. Across SMS, email, voice, and chat channels, the channel's effectiveness lies in its high engagement rate, allowing the debt collection text message to be read and responded to almost immediately.

However, the true optimization and the ability to scale this efficiency depend on Conversational AI (like Moveo.AI). The focus shifts from merely "sending a message" to "managing hundreds of thousands of humanized conversations 24/7".

In Moveo.AI's framing, this is the Customer-to-Cash loop in action. When the customer service team, AR team, and collections team all work from a single shared memory layer (TrueThread) and execute against a unified governance layer (TruePath), the message that reaches a delinquent customer reflects every relevant prior interaction: the support ticket they opened last week, the renegotiation they completed last quarter, the channel preference they expressed during onboarding.

This compounding context is the variable that separates 30% recovery from 60% recovery.

For context, Mobi2buy, in partnership with Moveo.AI, demonstrated the power of AI-driven conversational solutions by achieving an 80% increase in debt recovery compared to standard chatbots for one of the largest Telecom companies in Latin America, proving the channel's efficacy when powered by intelligence.

How to Optimize Debt Collection SMS/Text Messages

Human limitations in historical data retrieval, segmentation, and 24/7 communication prevent text message channels from reaching their full potential.

This is where Conversational AI is the ideal solution for the market's challenges of high volume and credit recovery.

Scalable Segmentation and Personalization

Function: The AI Agent retrieves the full delinquent customer history.

Benefit: It categorizes the customer (e.g., Recurring Payer, Long-Term Delinquent) and sends the most appropriate debt collection message (e.g., a discount proposal for a recurring customer, or a formal notice for a long-term delinquent). This ensures the message model is 100% personalized while maintaining scale.

Sentiment Analysis for the Ideal Response

Function: The AI understands the customer's communication sentiment (e.g., frustration, payment confirmation, negotiation request).

Benefit: If the customer responds with frustration, the agent can immediately redirect the conversation to an aggressive negotiation proposal or to a specialized human agent, preventing negative escalation and focusing on retention.

24/7 Availability with Immediate Response

Function: The AI responds instantly at any time.

Benefit: Debts are paid when the customer is available, maximizing recovery rates as payment opportunities are not lost outside of business hours.

Data Retrieval for Validation (FDCPA Compliance)

Function: The AI is connected to your management system (CRM/ERP). If the customer asks, "Where did this $[Amount] debt come from?", the AI instantly searches for and presents the precise information (e.g., August 2024 invoice, referring to the premium subscription).

Benefit: This resolves the core CFPB complaint (inaccurate debt), providing proof clearly and quickly, which increases trust and the likelihood of payment.

By adopting Conversational AI agents, you transform a manual and reactive process (with high risks of error and non-compliance) into a proactive, humanized, and highly scalable collection system. The result is optimized debt recovery, with debt collection text messages sample that not only collect but sell the payment solution.

Learn more ⭢ Understanding AI Collection Agents: Revolutionizing Debt Recovery

Measuring success: KPIs for debt collection messaging

High-performing collection operations track a defined set of metrics that go beyond simple payment rate. The five below form the minimum viable measurement set for evaluating whether a messaging strategy is improving.

Metric | What it measures and why it matters |

|---|---|

Response rate by channel and stage | Percentage of contacted accounts that respond (any inbound interaction). SMS typically generates 4 to 6 times the response rate of email; the gap widens as accounts age. Track this segmented by stage so changes in messaging strategy show up in the data. |

Payment rate per touch | Percentage of accounts that resolve within a defined window after a specific message touchpoint. Pre-due reminders typically convert 40 to 60% of eligible accounts. Late-stage messaging rarely exceeds 15% per touch even with strong settlement offers. |

Days-to-resolution | Average elapsed time from first message to payment or settlement. Operations that move from email-first to SMS-first cadences typically reduce this by 30 to 40% in the early stages. |

Net recovery rate | Percentage of total delinquent dollars recovered within a defined ageing bucket (30, 60, 90 days). The headline KPI of the operation; segments by message strategy reveal what's actually working at the portfolio level. |

Post-collection NPS or CSAT | Customer experience score collected after resolution. Operations that ignore this metric routinely recover the debt and lose the customer, producing a net negative on lifetime value. The goal is not to recover dollars at any cost; it is to recover dollars while preserving the future revenue stream. |

The most useful analyses cut these metrics by channel, stage, and debtor profile simultaneously.

The intersection of those three dimensions reveals where messaging strategy actually moves the needle, and where additional investment in personalization or automation has the highest marginal return.

The Intelligent Collection: From Confrontation to Humanized Conversation

The collection journey has evolved from a confrontation to a conversation. The strategic use of channels like WhatsApp, along with the implementation of advanced technologies like Conversational AI agents, allows you to deploy the ideal debt collection text message at the right time with the most efficient proposal.

By focusing on data accuracy (in line with best debt collection practices) and the humanization of dialogue, you not only improve your recovery metrics but also strengthen the long-term relationship with your customer.

Modern Customer-to-Cash operations connect customer service, accounts receivable, and collections into a single coordinated loop where every interaction informs the next. When a collection message reaches a customer who just opened a support ticket, or who renegotiated their account last month, or who asked to be contacted only after 6 p.m., the recovery stops being a confrontation and becomes a natural extension of the relationship.

This persistent memory across channels and functions, combined with deterministic, FDCPA- and Reg F-compliant execution, is what turns collections from a cost center into an operation that recovers dollars and preserves customer equity at the same time.

What is the next step to optimize your collections? Talk with an AI Expert, click here.